Why Projecting Revenue Metrics Onto Tokens is Financial Theater

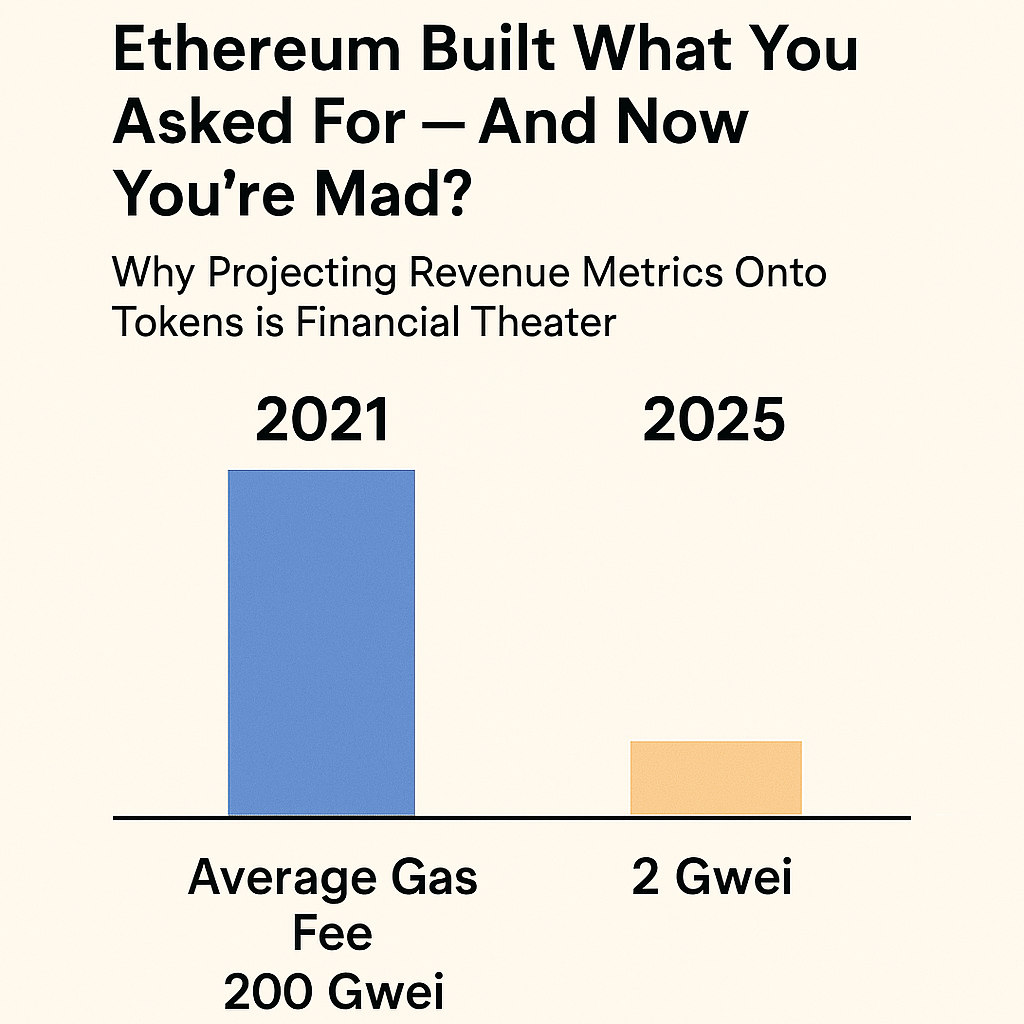

Remember 2021? When sending a simple ERC-20 transfer on Ethereum cost more than your coffee? Back then, crypto Twitter was ablaze with outrage—“Ethereum is unusable,” “We need cheaper transactions,” “This won’t scale.”

Fast forward to 2025. Ethereum listened. Developers shipped. Upgrades like EIP-1559, The Merge, and most recently Dencun brought average gas fees from triple-digit Gwei levels down to mere single digits. The network scaled horizontally via rollups, while danksharding and blobspace made things even cheaper.

Now… enter the finance bros. The same crowd that wouldn’t touch Ethereum at $200 because “no cash flows” are suddenly fixated on ETH at $3,500—but not for the reasons you’d think.

“Lower gas fees = less revenue. Why such a high valuation?”

This line of questioning is becoming common. It’s also fundamentally flawed.

The Misguided “Token-as-Equity” Framework

ETH isn’t a stock. It doesn’t issue dividends. It’s not a “company.” Yet increasingly, people treat blockchains like cash-flow businesses: comparing validator revenue to company income, measuring “network value to transaction ratio,” and applying DCF models to tokenomics.

While there is some intellectual value in understanding incentives, calling reduced gas fees a “revenue hit” misses the forest for the trees.

Ethereum didn’t kill gas fees because it wanted to reduce “revenue.” It did so because the network was so called unusable for the majority of people. Lower gas fees = more users = greater utility = stronger demand for blockspace. That’s positive-sum.

ETH’s Value Isn’t About Revenue

ETH is ultrasound money. It’s a commodity asset that secures the network. It’s collateral. It’s settlement. It’s access to blockspace. None of those things are easily measurable via traditional P&L metrics. Trying to force equity-style frameworks onto ETH is like asking why gold doesn’t issue quarterly reports.

What matters is the total economic bandwidth of Ethereum. The more people using it, the more things built on it, the stronger the narrative—and the more valuable ETH becomes as a foundational asset.

Irony: Ethereum Did Its Job Too Well

The irony is rich: Ethereum was penalized in 2021 for being too expensive. Now, it’s being “penalized” again in 2025 for being too cheap. But cheapness was the goal. Scalability was the milestone. And blockchains aren’t SaaS companies.

The real question isn’t “why is ETH still valued highly despite less fee revenue?”

It’s: “Why are we still projecting TradFi metrics onto a fundamentally different paradigm?”

TLDR

- Ethereum gas fees dropped ~95% from 2021 to 2025. Mission accomplished.

- Finance bros now use “revenue” as a critique, forgetting ETH isn’t a company.

- Projecting equity-style valuations onto blockchains misunderstands their nature.

- Ethereum is a public utility. Its native asset is tied to utility and security—not profit margins.

- ETH is money. Treat it like money.